Meaning of “Specified Person” under Section 194S

A “specified person” means:

An individual or a Hindu Undivided Family (HUF) who does not have income under the head “Profits and Gains of Business or Profession” (i.e., salaried persons, pensioners, etc.).

OR

An individual or HUF whose income does include business/professional income. But whose total sales/gross receipts/turnover from business or profession in the preceding financial year are ≤ ₹1 crore (for business) or ≤ ₹50 lakhs (for profession).

In other words:

If you are a salaried person with some investments in crypto (no business income), you are a specified person.

If you run a small business or profession but last year’s turnover was within the above limits, you are still a specified person.

If your turnover last year exceeded ₹1 crore (business) or ₹50 lakh (profession), you are not a specified person → so only the ₹10,000 threshold applies.

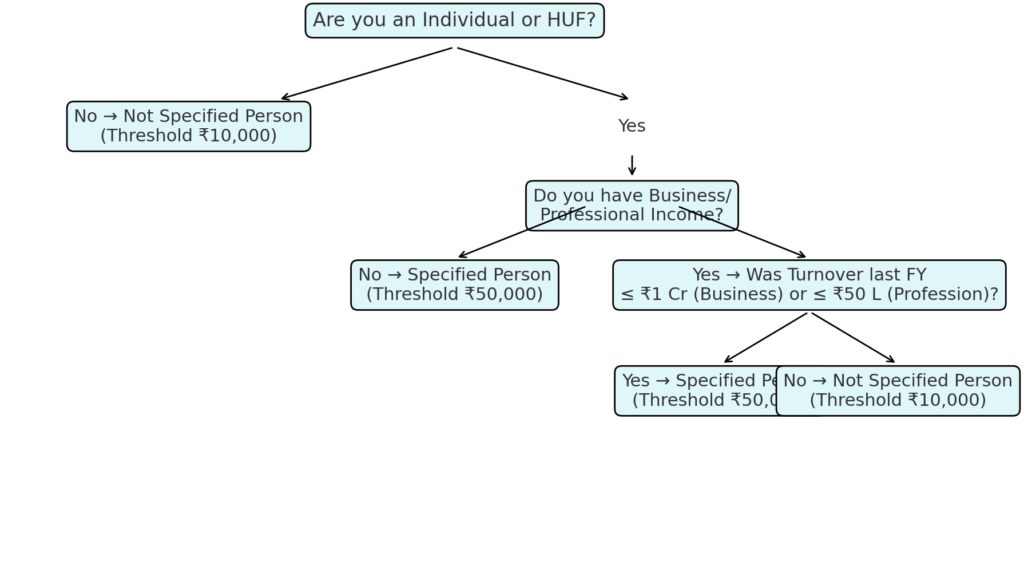

Here’s a quick checklist to determine whether you (or a client) qualify as a “Specified Person” under Section 194S (VDA TDS):

✅ Specified Person Checklist

- Are you an individual or an HUF?

- ❌ If No → You are NOT a specified person → Threshold = ₹10,000

- ✅ If Yes → Go to Q2

- Do you have Business or Professional Income?

- ❌ If No → You are a Specified Person → Threshold = ₹50,000

- ✅ If Yes → Go to Q3

- If Yes, was your turnover/gross receipts in the preceding FY:

- ≤ ₹1 crore (Business), or

- ≤ ₹50 lakhs (Profession)?

- ✅ If Yes → You are a Specified Person → Threshold = ₹50,000

- ❌ If No → You are NOT a specified person → Threshold = ₹10,000

👉 Shortcut Rule:

- Most salaried individuals / investors = Specified Person (₹50k threshold)

- Large businesses / professionals above limits = Not Specified (₹10k threshold)